Paper/Subject Code: 46009/Finance: Wealth Management

TYBMS SEM :5

Finance :

Wealth Management

(Q.P. November 2024 with Solution)

.png)

Note:

1) All questions are compulsory subject to internal choice.

2) Figures to the right indicate full marks.

3) Use of simple calculator is allowed

Q.1. (a) Multiple Choice Questions: (any 8) (08)

1. _______ planning is a way by which you can reduce your tax liability without breaking up any law.

a) Goal

b) Management

c) Tax

d) Currency

2. ________ means marketability of an investment.

a) Planning

b) Liquidity

c) Saving

d) Crediting

3. Accumulation of assets which generate income period of time means ________.

a) Wealth Creation

b) Saving

c) Planning

d) None of the above

4. The term ________ consists of owned by you at the time of your death.

a) Will

b) Career

c) Estate

d) Trust

5. _______ analysis help to know the liquidity position of the company.

a) Cash Flow

b) Expenses flow

c) Real Estate

d) Gross Profit

6. ________ funds are a relatively new approach to retirement investing.

a) Goal Based

b) Optimal

c) Life Cycle

d) None of the above

7. Health Insurance premium provide tax exemption under section ________ Income Tax.

a) 80 A

b) 80C

c) 80 D

d) 80 G

8. ________ applies to debt investment such as bonds.

a) Debit risk

b) Planned risk

c) Currency risk

d) Credit risk

9. _______ insurance principle means both the insured and the have faith in each other.

a) Principle of Indemnity

b) Principle of utmost good faith

c) Principle of contribution

d) Principle of sharing

10. The yield curve is ________ when yield of a s are close to one another.

a) Downward sloping

b) Humped

c) Upward sloping

d) Flat

b) State whether the following statements are true or false: (any 7) (07)

1. CAGR return is same as Holding period return

Ans: False

2. Estate planning is concerned with ensuring adequate coverage against insurable risks.

Ans: False

3. Net worth Assets + Liabilities.

Ans: False

4. Wealth management is a one-time solution to achieving financial goals.

Ans: False

5. Longevity risk is the risk of outliving your savings.

Ans: True

6. Ratio analysis is an important technique of financial statement analysis.

Ans: True

7. Subrogation is principle, which applied to all contracts of indemnity.

Ans: True

8. Equity risk applies to an investment in shares

Ans: True

9. If the interest rate goes up, the market value of bonds will decrease.

Ans: True

10. Passive management strategies are tax-efficient.

Ans: True

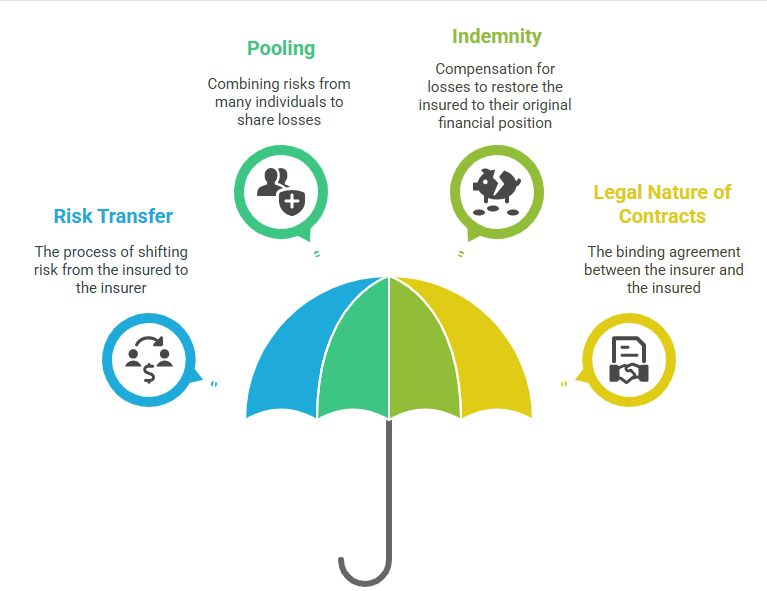

Q.2 a) Explain the characteristics of Insurance. (08)

Insurance is a financial mechanism that provides protection against potential future losses or risks. It plays a crucial role in risk management for individuals and businesses alike. This document outlines the key characteristics of insurance, highlighting its fundamental principles and functions.

1. Risk Transfer

One of the primary characteristics of insurance is the transfer of risk from the insured to the insurer. By purchasing an insurance policy, individuals or businesses shift the financial burden of potential losses to the insurance company. This allows policyholders to manage their risks more effectively.

2. Pooling of Risks

Insurance operates on the principle of pooling risks. Insurers collect premiums from a large number of policyholders, creating a pool of funds. This pool is then used to pay for the claims of those who experience losses. The pooling of risks helps to spread the financial impact of losses across many individuals, making it more manageable.

3. Premium Payment

To obtain insurance coverage, policyholders must pay a premium. This is a regular payment made to the insurer in exchange for the promise of financial protection. The amount of the premium is determined by various factors, including the level of coverage, the type of insurance, and the risk profile of the insured.

4. Indemnity

Insurance is based on the principle of indemnity, which means that the insured should be restored to their financial position prior to the loss, without making a profit from the insurance claim. This characteristic ensures that insurance serves as a safety net rather than a source of profit.

5. Uncertainty and Contingency

Insurance deals with uncertain events that may or may not occur in the future. The very nature of insurance is to provide coverage against unforeseen circumstances, such as accidents, natural disasters, or health issues. This characteristic highlights the importance of contingency planning in risk management.

6. Legal Contract

An insurance policy is a legal contract between the insurer and the insured. It outlines the terms and conditions of coverage, including the rights and responsibilities of both parties. This contract is enforceable by law, providing a framework for resolving disputes and claims.

7. Underwriting

Underwriting is the process by which insurers assess the risk associated with insuring a particular individual or entity. This involves evaluating various factors, such as health, lifestyle, and financial history, to determine the appropriate premium and coverage. Effective underwriting helps insurers maintain financial stability.

8. Regulation

The insurance industry is heavily regulated to protect consumers and ensure fair practices. Regulatory bodies oversee the operations of insurance companies, ensuring they maintain adequate reserves to pay claims and adhere to ethical standards. This characteristic fosters trust and confidence in the insurance system.

b) What is estate planning? What are the tools of estate planning? (07)

Estate planning is a crucial process that involves preparing for the management and distribution of an individual's assets after their death or in the event of incapacitation. It ensures that a person's wishes regarding their property, finances, and healthcare decisions are honored, while also minimizing taxes and legal complications for heirs. This document explores the fundamental concepts of estate planning and outlines the various tools available to facilitate this important process.

What is Estate Planning?

Estate planning is the strategic arrangement of an individual's financial and legal affairs to ensure that their assets are distributed according to their wishes upon death or incapacitation. It encompasses a variety of considerations, including the management of assets, the appointment of guardians for dependents, and the establishment of healthcare directives. The primary goal of estate planning is to provide peace of mind, protect loved ones, and ensure that one's legacy is preserved.

Tools of Estate Planning

There are several essential tools that individuals can utilize in their estate planning efforts. Each tool serves a specific purpose and can be tailored to meet individual needs:

1. Wills

A will is a legal document that outlines how a person's assets will be distributed after their death. It allows individuals to specify beneficiaries, appoint an executor, and designate guardians for minor children. Wills are fundamental to estate planning and can help avoid disputes among heirs.

2. Trusts

Trusts are legal arrangements that allow a third party, known as a trustee, to hold and manage assets on behalf of beneficiaries. There are various types of trusts, including revocable living trusts, irrevocable trusts, and special needs trusts. Trusts can help minimize estate taxes, avoid probate, and provide for specific needs of beneficiaries.

3. Powers of Attorney

A power of attorney (POA) is a legal document that grants someone the authority to make decisions on behalf of another person in financial or legal matters. This tool is essential for ensuring that an individual's affairs are managed according to their wishes if they become incapacitated.

4. Healthcare Directives

Healthcare directives, also known as advance directives or living wills, specify an individual's preferences regarding medical treatment and end-of-life care. These documents ensure that healthcare decisions align with the individual's values and desires when they are unable to communicate their wishes.

5. Beneficiary Designations

Many financial accounts, such as retirement plans and life insurance policies, allow individuals to designate beneficiaries. These designations override wills and ensure that assets are transferred directly to the named beneficiaries upon death, bypassing probate.

6. Gift Planning

Gift planning involves making gifts during a person's lifetime to reduce the size of their estate and potentially minimize estate taxes. This can include cash gifts, property transfers, or contributions to charitable organizations.

7. Estate Tax Planning

Estate tax planning focuses on strategies to minimize the tax burden on an estate. This can involve the use of trusts, gifting strategies, and other financial tools to ensure that more of an individual's wealth is passed on to heirs rather than being consumed by taxes.

OR

c) Find out the net taxable income of Mr. Krishnam for AY 2025-26 applying the provisions of set off and carry forward of losses.

|

Particulars |

Amount |

|

Income from Salary |

2,20,000 |

|

Income from House Property: |

|

|

Loss from Parel house |

(1,00,000) |

|

Income from Dadar house |

50,000 |

|

Income from Juhu house |

30,000 |

|

Income from business: |

|

|

Business I (speculative) |

40,000 |

|

Business II (non-speculative) |

75,000 |

|

Business III (non-speculative) |

(25,000) |

|

Income from capital gain: |

|

|

Income from log term capital gains |

60,000 |

|

Short term capital loss |

(45,000) |

|

Income from other sources: |

|

|

Interest on debentures |

5,000 |

|

Interest on Bank fixed deposits |

20,000 |

Additional information:

a. Rs. 1,500/- spent on collection towards interest on debenture (Allowed under section 57 as expenditure.

b. Carry forward speculative business losses Rs. 55,000/- (AY 2022-23)

c. Carry forward long term capital losses Rs. 70,000/-(AY 2021-22)

Q.3 a) Explain the requirement of goal based financial planning and its advantages. (08)

Goal-based financial planning is a strategic approach that focuses on defining specific financial objectives and creating a tailored plan to achieve them. This method emphasizes the importance of aligning financial decisions with personal goals, whether they are short-term, medium-term, or long-term. By prioritizing individual aspirations, goal-based financial planning helps individuals and families navigate their financial journeys more effectively. This document explores the requirements of goal-based financial planning and highlights its numerous advantages.

Requirements of Goal-Based Financial Planning

Clear Goal Definition: The first step in goal-based financial planning is to clearly define financial goals. These can include saving for retirement, purchasing a home, funding education, or planning for vacations. Each goal should be specific, measurable, achievable, relevant, and time-bound (SMART).

Comprehensive Financial Assessment: A thorough evaluation of current financial status is essential. This includes analyzing income, expenses, assets, liabilities, and existing investments. Understanding one’s financial situation provides a solid foundation for planning.

Prioritization of Goals: Not all goals hold the same weight. It’s crucial to prioritize them based on urgency and importance. This helps in allocating resources effectively and ensures that critical goals are addressed first.

Investment Strategy Development: Based on the defined goals and financial assessment, a tailored investment strategy should be developed. This strategy should consider risk tolerance, time horizon, and the expected rate of return needed to achieve the goals.

Regular Monitoring and Adjustment: Financial planning is not a one-time event. Regular monitoring of progress towards goals is necessary, along with adjustments to the plan as circumstances change, such as income fluctuations, market conditions, or shifts in personal priorities.

Advantages of Goal-Based Financial Planning

Enhanced Focus and Motivation: By having specific goals, individuals are more likely to stay focused and motivated to save and invest. This clarity helps in making informed financial decisions that align with their aspirations.

Improved Financial Discipline: Goal-based planning encourages disciplined saving and spending habits. Individuals are more likely to stick to their budgets and avoid unnecessary expenditures when they have clear objectives in mind.

Tailored Financial Solutions: This approach allows for customized financial strategies that cater to individual needs and circumstances. It ensures that financial products and services are aligned with personal goals, leading to better outcomes.

Increased Accountability: Setting clear goals creates a sense of accountability. Individuals are more likely to track their progress and make necessary adjustments to stay on course, fostering a proactive approach to financial management.

Reduced Financial Stress: Knowing that there is a structured plan in place to achieve financial goals can significantly reduce anxiety and stress related to money management. It provides a sense of control and confidence in one’s financial future.

Long-Term Financial Security: Goal-based financial planning promotes a long-term perspective on wealth accumulation and preservation. By focusing on future objectives, individuals are more likely to make decisions that contribute to lasting financial security.

b) Describe wealth management process. (07)

Wealth management is a comprehensive approach to managing an individual's or family's financial resources to achieve specific financial goals. This document outlines the key components of the wealth management process, which typically includes assessment, planning, implementation, and ongoing management. Understanding this process is crucial for individuals seeking to optimize their financial health and ensure long-term prosperity.

1. Assessment

The first step in the wealth management process is a thorough assessment of the client's current financial situation. This includes:

Financial Goals: Identifying short-term and long-term financial objectives, such as retirement planning, education funding, or estate planning.

Net Worth Analysis: Evaluating assets, liabilities, and overall net worth to understand the financial landscape.

Risk Tolerance: Assessing the client's willingness and ability to take risks with their investments, which will influence the investment strategy.

2. Planning

Once the assessment is complete, the next step is to develop a comprehensive financial plan tailored to the client's needs. This phase includes:

Investment Strategy: Creating a diversified investment portfolio that aligns with the client's risk tolerance and financial goals.

Tax Planning: Implementing strategies to minimize tax liabilities and maximize after-tax returns.

Retirement Planning: Establishing a plan for retirement income, including Social Security, pensions, and personal savings.

Estate Planning: Developing a strategy for wealth transfer to heirs, including wills, trusts, and other estate planning tools.

3. Implementation

After the financial plan is developed, the next step is to put the plan into action. This involves:

Investment Execution: Buying and selling assets according to the agreed-upon investment strategy.

Insurance Coverage: Securing appropriate insurance policies to protect against unforeseen events that could impact financial stability.

Account Management: Setting up and managing various accounts, such as brokerage accounts, retirement accounts, and savings accounts.

4. Ongoing Management

Wealth management is not a one-time event; it requires continuous monitoring and adjustments. This phase includes:

Performance Review: Regularly reviewing the performance of investments and the overall financial plan to ensure alignment with goals.

Rebalancing: Adjusting the investment portfolio as needed to maintain the desired asset allocation and risk level.

Adaptation: Making changes to the financial plan in response to life events, market conditions, or changes in financial goals.

OR

c) Mr. Kantilal purchased a house property for Rs. 18,00,000 on 1 June, 1993. He incurred expenses of Rs, 6,50,000 in financial year 1998-99 and Rs. 8,70,000 in the financial year 2006-07.

The fair market value if the property on 1 April, 2001 was Rs. 27,00,000. He sold the property on 1" October, 2022 for Rs. 1,75,00,000. Brokerage of Rs. 1,50,000 was incurred on sale transaction. He purchased a new residential house on 1 January, 2023 for Rs. 13,00,000. (08)

Cost inflation index: 2001-02 = 100, 2006-07 = 122, 2022-23 = 331.

Calculate capital gain for the year 2022-23.

Elective: Logistics & SCM (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: CC & PR (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | Solution | |

2024 | Nov | ||

2025 | April | Solution | |

Elective: Finance: IAPM (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: Marketing: Service Marketing (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: HR : Finance for HR Professional & Compensation Management (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: Finance : Commodity & Derivatives (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | Solution | |

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: Marketing : E-Commerce & Digital Marketing (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: HR : Strategics HRM (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | Solution | |

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: Marketing : Sales & Distribution (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: HR : Performance Management & Career Planning (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | Solution | |

2025 | April | Solution | |

Elective: Finance : Financial Accounting (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | Solution | |

2019 | Nov | ||

2022 | Nov | ||

2023 | April | Solution | |

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: Marketing : Customer Relationship Management (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | Solution | |

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: Human Resource: Industrial Relation (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| |

2018 | Nov | Solution | |

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | Solution | |

2025 | April | Solution | |

Elective: Finance : Risk Management (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | Solution | |

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

Elective: Finance : Wealth Management (CBCGS) | |||

Year | Month | Question Papers | Link |

IMP Q. |

|

| Solution |

2018 | Nov | ||

2019 | April | ||

2019 | Nov | ||

2022 | Nov | ||

2023 | April | ||

2023 | Nov | ||

2024 | Nov | ||

2025 | April | Solution | |

.png)

.png)

.png&description=TYBMS SEM :5 Finance : Wealth Management (Q.P. November 2024 with Solution)){kind=link}

0 Comments